Discussion of

"Liquidity Mechanisms in DeFi: Design and Fragmentation in Illiquid RWA Markets"

by Ralf Laschinger, Heiko Leonhard, Gregor Dorfleitner, and Wolfgang Schäfers

Discussant: Katya Malinova

DeGroote School of Business, McMaster University

CBER 6th Annual Conference · June 4–5, 2026

New York University, New York, NY, USA

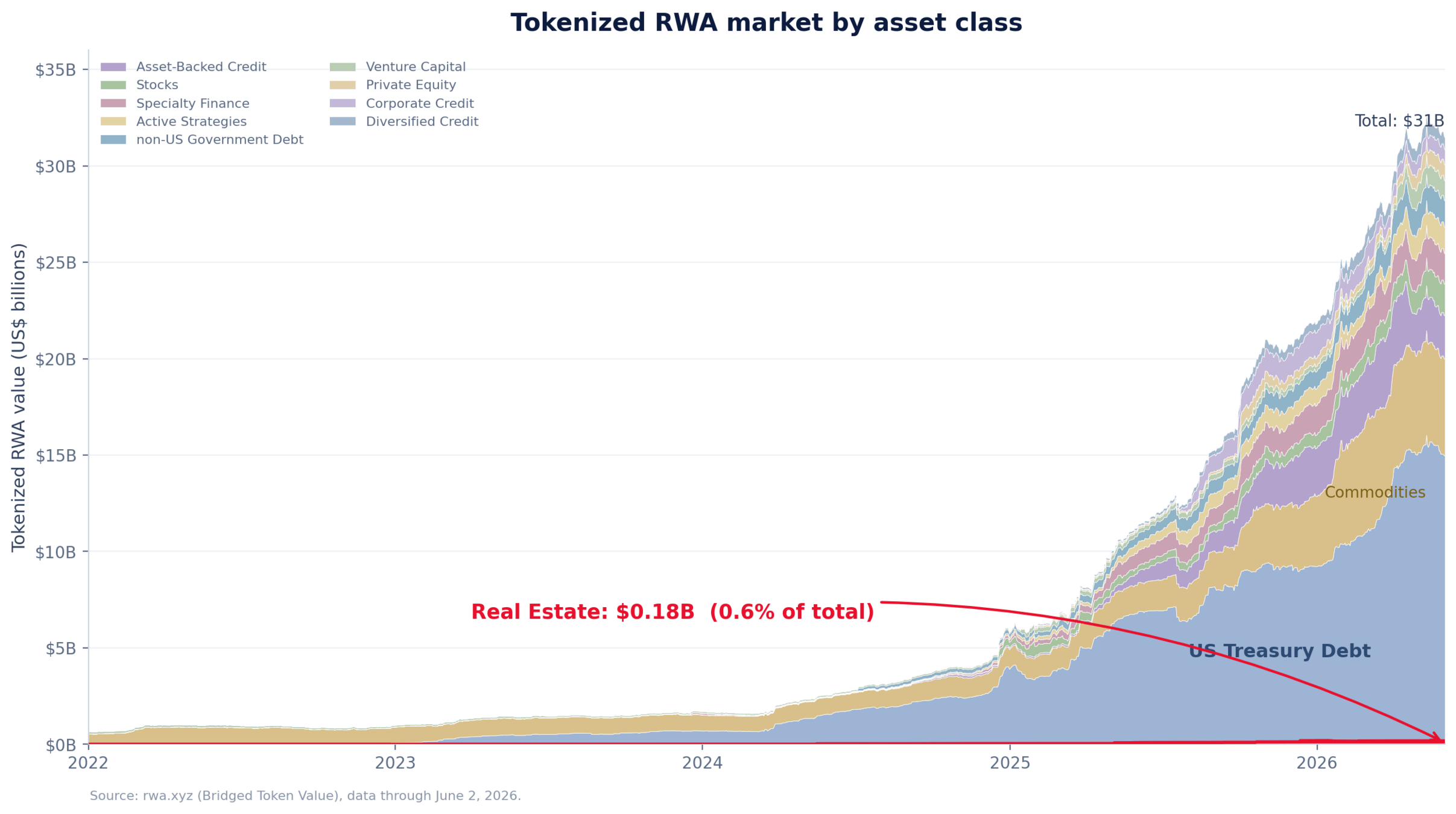

Tokenized RWA. Fractional. Tradable. Liquid?

- US real estate: $55T

- REITs: $1.4T

- tokenized: ~$0

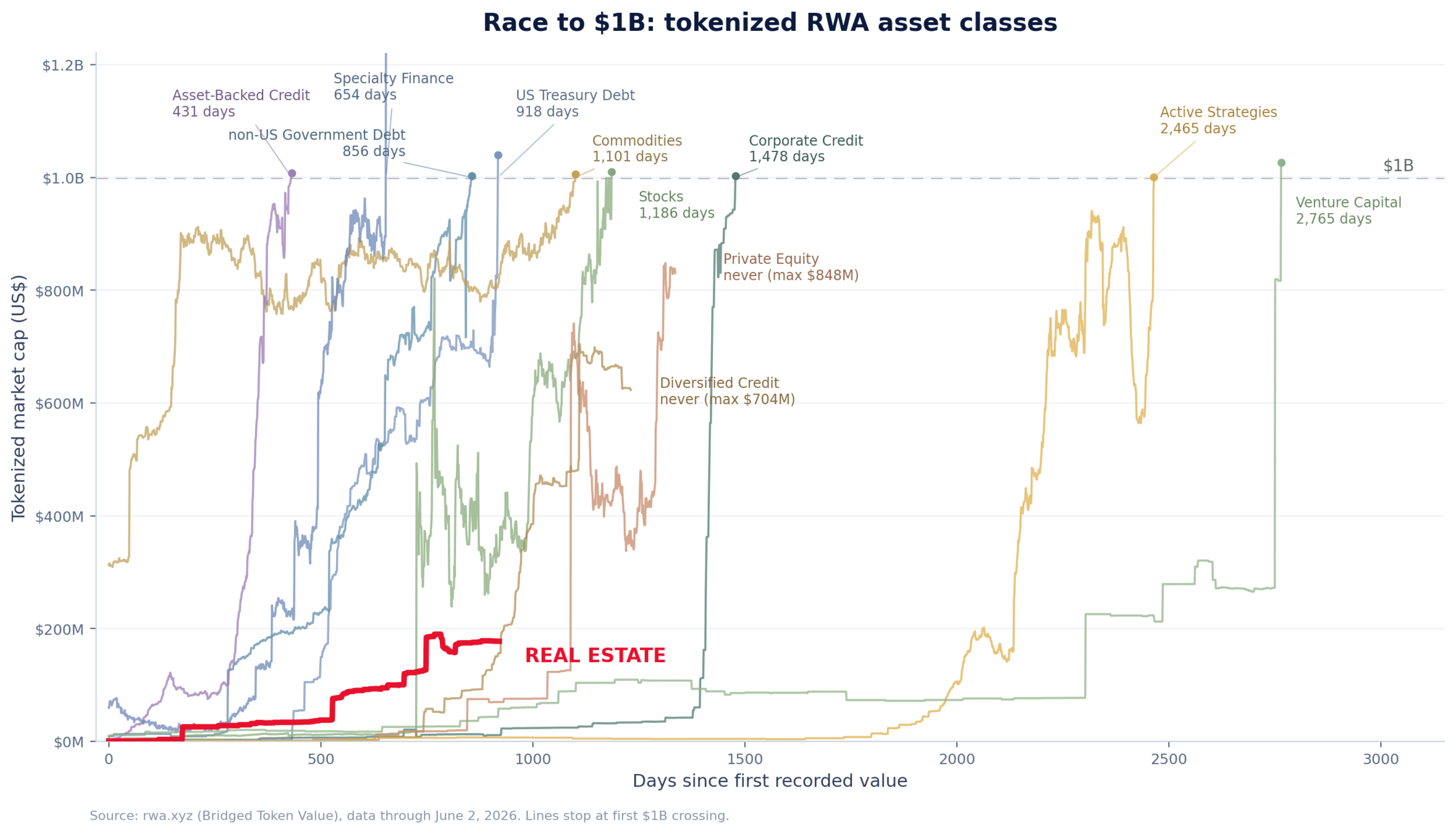

June 2, 2026 updated version of a Chainalysis blog figure

Market cap growth of tokenized RWA asset classes - to $1 Billion

Not all RWAs are created equal

… nor supposed to — Cong, Mayer & Rabetti (2026):

Different tokenization goals

Integration

already-liquid assets join the on-chain ecosystem

Enhance transferability

creating a secondary market

This paper's focus

Why expect tokenization to beget liquidity?

- Divisibility/Fractional Ownership - akin to stock splits

- Apple Inc. 2014, 7-for-1, $645 → $92

- "to make Apple stock more accessible to a larger number of investors"

- (Easy) Tradability:

- Tel Aviv: corporate bonds trade in a limit order book & very liquid (Abudy & Wohl, RoF 2018)

- Yet RealT: little liquidity, little activity

- ~9,200 wallets

- $41M traded in six years

- $9K per property per year

- Too early? No trust in "tokenized"?

- Is it the organization (and fragmentation) of trading?

- Or is it the asset itself?

Six-year stats:

- 752 rental properties

- ~9,200 wallets

- 777,038 trades — ≈ $50 each

- $41M — $9K per property/yr

REITs democratized access in 1960. What do tokens add (undo)?

| Problem | REIT | Property token |

| Huge lot size → fractional claims | ✓ | ✓✓ $50 of a house |

| Hard to trade, limited access → democratize access | ✓ | ✓✓ anyone*, anywhere* |

| Locked-in capital → tradability | ~ ✓ | ✓✓ 24/7 |

| Idiosyncratic risk → pooling | ✓ | ~ ✓ DIY |

| Hands-on management → professional, monitored mgmt | ✓ | ~ outsourced but who monitors? |

| Unverified valuation → audited disclosure | ✓ | ~ issuer-reported, periodic |

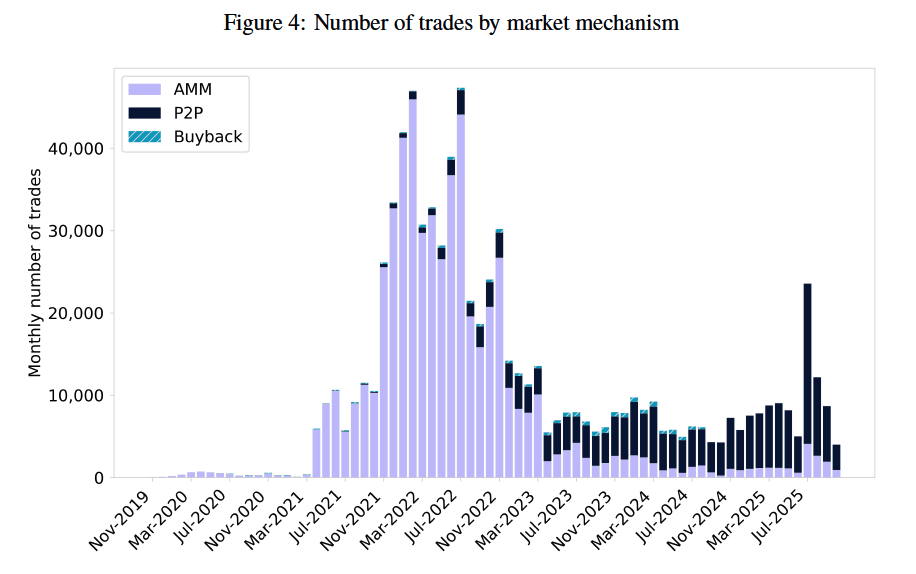

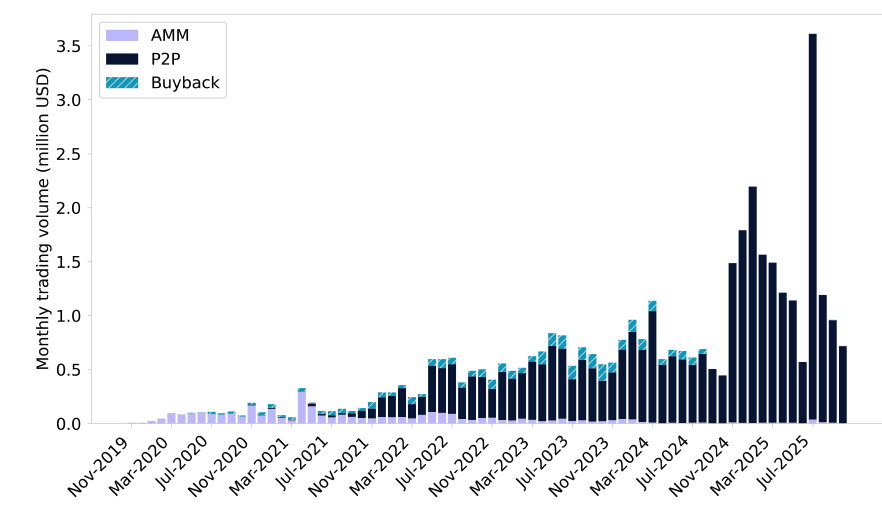

Transferrable? And where? AMM, P2P, or Buyback?

- Sorting?

- AMM = small, P2P = large

- LOB vs "upstairs" (blocks)

- venue pecking order: Menkveld, Yueshen & Zhu 2017 JFE (execution vs cost)

- Or: winner takes all?

- liquidity begets liquidity → one venue (Pagano 1989 QJE)

- Here: looks like one venue winning

Is this bad news for AMMs? Not necessarily ...

- AMM design — active research.

- **E.g. on LP compensation (= AMM fee):

- Hasbrouck, Rivera & Saleh (MS 2026):

- ↑ fee → deeper pool → ↓ price impact → ↑ volume

- Malinova and Park 2026 "Learning from DeFi ...":

- AMM fee ∝ σ · √(q/V) — ↑ volatility, ↓ volume

- Hasbrouck, Rivera & Saleh (MS 2026):

- Here: 0.25%, hardcoded

- AMM fees not enough compensation → issuer pays incentives to LPs

- incentives stop → liquidity gone (not unique to AMM ... Park & Stinner 2026, DeFi lending)

**with apologies to the many others in this literature, many in this room

... But: is Real Estate built for 24/7 trading? (after Fig. 2 Cong, Mayer & Rabetti WP)

Asset value adjustment speed ↑

Underbuilt

Permissioned wholesale pilots on liquid assets

Integration benefits forgone

Well matched (fast)

Tokenized Treasuries, equities

Well matched (slow)

Closed-end, gated, or lock-up tokenized illiquid vehicles

Speed-mismatched - liq transformation

Real Estate!

Buy&Hold in normal times - run risk under stress (Blackstone REIT: gated withdrawals 2022–23)

corp. bond ETFs — same mismatch, but professionally managed: Koont, Ma, Pástor & Zeng, RFS 2025

Trading speed →

But: corp bonds are very liquid in a Tel-Aviv LOB (Abudy & Wohl, RoF 2018). Why?

Transparent ownership, Opaque control

July 2025: TRO — rent → escrow, Buyback suspended

- Paper: "a shock to the redemption facility"

- but — also news about the asset itself!

- can we disentangle? The size split helps (?)

- spreads widen for large, narrow for small

More questions arise:

- dispersed ownership — agency problem?

- a mechanism against tokenized lemons?

Mortgage Professional America, July 7, 2025

Added ex post (web version): two papers I learned of only after the session, both directly relevant:

• Augustin, Chen, Qian & Shin (2025), From Bricks to Blocks: Tokenization and the Financialization of Real Estate

• Chemla & Tinn (2026), Digital Ownership: The Tokenization of Real-World Assets

Better rails don't automatically createreinvent

liquidity, information, nor governance.

Very nice paper.

Go read it.