Book 4. Liquidity and Treasury Risk

FRM Part 2

LTR 13. Repurchase Agreements and Financing

Presented by: Sudhanshu

Module 1. Mechanics of Repos, Repo Motivations, and Counterparty and Liquidity Risk

Module 2. Recent Credit Crisis, Collateral and Special Spread

Module 1. Mechanics of Repos, Repo Motivations, and Counterparty and Liquidity Risk

Topic 1. Mechanics of Repurchase Agreements

Topic 2. Borrowers in Repos

Topic 3. Lenders in Repos

Topic 4. Counterparty Risk and Liquidity Risk

Topic 1. Mechanics of Repurchase Agreements

- A repurchase agreement (repo) is a contract where one party sells a security with a promise to buy it back at a future date at a higher price.

-

The difference between the sell and buy prices of the security is the implied interest (i.e., return) on the transaction.

- From the perspective of the borrower, it is a repo; from the perspective of the lender, it is a reverse repo.

- Economically, it is a short-term secured by collateral.

-

Repos are used by:

-

Borrowers who need short-term funds, and

-

Lenders who need short-term investments or access to collateral.

-

Topic 1. Mechanics of Repurchase Agreements

-

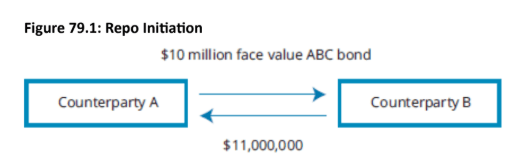

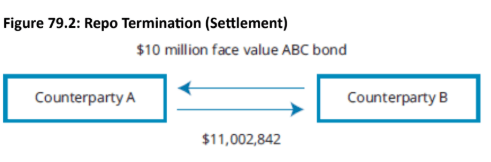

Settlement Calculation: The repurchase price is calculated using the initial loan amount, the annualized repo rate, and the days to maturity. Repo rates typically use an actual/360-day count.

-

-

-

-

Example: For a $11,000,000 loan over 31 days at a 0.3% annual rate, the repurchase price would be:

-

-

\text { Repurchase Price }=\text { Initial Loan Amount } \times\left(1+\frac{\text { Annual Repo Rate } \times \text { Days to Maturity }}{360}\right)

\$ 11,000,000 \times\left(1+\frac{0.3 \% \times 31}{360}\right)=\$ 11,002,841.67

Practice Questions: Q1

Q1. Pasquini Investments (Pasquini) is a private brokerage looking for 30-day financing of $25 million of its accounts payable but is unsure whether the appropriate investment is a term repurchase agreement (repo) or a term reverse repo agreement. Pasquini is willing to post AAA-rated government bonds as collateral. The bonds have a face value of $27 million and a market value of $25 million. The firm is quoted a rate of 0.5% for the transaction. Which of the following choices most accurately reflects the contract type and the contract price needed by Pasquini?

Practice Questions: Q1 Answer

Explanation: C is correct.

Given that Pasquini is a borrower in the repo market, the transaction is a repo from the perspective of the firm (but a reverse repo from the perspective of the lender). The contract price is calculated as follows:

\$ 25,000,000 \times\left(1+\frac{0.5 \% \times 30}{360}\right)=\$ 25,010,417

Topic 2. Borrowers in Repos

-

Low-cost short-term funding: From the borrower’s perspective, repos provide a relatively cheap way to raise short-term funds compared to unsecured borrowing.

-

Favorable rates: As the borrowing is collateralized, lenders accept lower returns in exchange for reduced credit risk, resulting in more attractive funding rates.

-

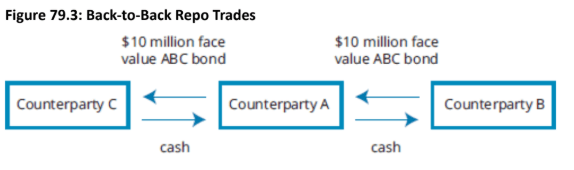

Financing bond positions or inventory:

-

Financing long security positions: Repos allow financial institutions to finance bond purchases by borrowing short-term cash and pledging the purchased security as collateral, subject to haircuts.

-

Rolling and inventory financing: If the position cannot be closed immediately, the repo must be rolled, either with the same counterparty or by unwinding and re-entering with a new one.

-

The same mechanism is used to finance proprietary positions and trading inventory for market making.

-

Topic 2. Borrowers in Repos

-

Liquidity Management:

-

Funding choices and stability trade-off: Firms can raise funds via equity or debt (secured or unsecured).

-

Repos provide cheap, secured short-term funding but are less stable due to rollover risk and sensitivity to market conditions

-

Equity is the most stable but also the most expensive form of financing.

-

-

Liquidity management: Firms must balance funding cost against stability and refinancing risk across instruments to avoid funding shortfalls

-

This balancing act is central to effective liquidity management.

-

-

Topic 3. Lenders in Repos

-

Cash Management:

-

Short-term investment of surplus cash: Lenders use reverse repos to earn returns on excess cash held for liquidity or safekeeping, rather than leaving it idle.

-

Low-risk, collateralized option: Entities such as money market funds and municipalities prefer repos because they offer short maturities, collateral security, and low risk while complying with conservative investment constraints.

-

Investors preference: Investors prefer high liquid and high quality collaterals with low haircuts.

-

-

Short Position Financing:

-

Financing bond short positions: Lenders can use reverse repos to obtain bond collateral by lending cash, enabling them to short-sell the bond when they expect prices to fall (e.g., due to rising interest rates).

-

Profit mechanism and flows: The bond obtained via reverse repo is sold and later repurchased at a lower market price, with transaction flows mirroring standard repo mechanics, but with the lender acting as the reverse repo counterparty.

-

Topic 4. Counterparty Risk and Liquidity Risk

- Repo transactions involve the exchange of cash and collateral. Accordingly, it gives rise to both liquidity risk and counterparty credit risk.

-

Counterparty credit risk: Counterparty credit risk arises from the borrower’s potential default.

-

It is mitigated in repos because the loan is collateralized and typically short term, allowing the lender to recover amounts owed by selling the collateral.

-

-

Liquidity risk of collateral: Even with low credit risk, lenders face liquidity and market value risk of the collateral, especially during market stress.

-

It is managed through haircuts, margin calls, shorter repo tenors, and acceptance of high-quality collateral.

-

Practice Questions: Q2

Q2. Posting collateral and requiring collateral haircuts are important risk mitigants in repo transactions with respect to which of the following risks?

Practice Questions: Q2 Answer

Explanation: D is correct.

Collateral is an important counterparty credit risk mitigant. Repo loans are secured by collateral, which makes the lender much less vulnerable to a decline in the credit worthiness of the borrower. Collateral haircuts are important in mitigating liquidity risk in repo transactions. The lender is exposed to the risk of the value of the collateral declining during the repo term, which can be mitigated by requiring (higher) haircut values, that is, discounts to the value of the posted collateral.

Practice Questions: Q3

Q3. Kotra Bank Holdings, Inc., (Kotra) is currently weighing the cost of its funding against the risk of being left without financing. The term that best describes Kotra’s activities is:

A. counterparty (credit) risk.

B. specials trading.

C. liquidity management.

D. overnight funding.

Practice Questions: Q3 Answer

Explanation: C is correct.

The process of weighing the cost of its funding against the risk of being left without financing is called liquidity management. Counterparty (credit) risk is the risk of borrower default or non-payment of its obligations. In specials trading, a lender of cash initiates a repo trade in order to receive a particular security (special collateral). Overnight funding refers to borrowing and lending in the overnight market.

Module 2. Recent Credit Crisis, Collateral and Special Spread

Topic 1. Repos During the Credit Crisis

Topic 2. Collateral in Repo Transactions

Topic 3. Special Spreads and the Auction Cycle

Topic 4. Special Spreads and Rate Levels

Topic 5. Financing Advantage of a Bond Trading Special

Topic 1. Repos During the Credit Crisis

-

Pre- GFC crisis conditions: Before the 2007–2009 crisis, repo markets were liquid, with stable participation and widespread acceptance of lower-quality collateral in exchange for higher repo rates.

-

Crisis dynamics: As stress intensified, lenders demanded higher-quality collateral and larger haircuts, and in some cases withdrew liquidity altogether.

-

Consequences: The sudden loss of repo funding triggered collateral liquidations, capital erosion, and bankruptcies, as seen in the failures of Lehman Brothers and Bear Stearns.

-

Lehman Brothers:

- Tri-party repo structure: JPMorgan acted as Lehman’s tri-party repo clearing agent, managing collateral, settlement, and payments for overnight repos without taking direct transaction risk, while also providing intraday secured funding.

-

Rising haircuts and exposure: As repo market stress intensified in 2008, JPM began imposing haircuts on intraday loans, with exposures exceeding $100 billion in the final week before Lehman’s bankruptcy.

-

Disputed actions before failure: Lehman accused JPM of exploiting its dual role as agent and lender to extract nearly $14 billion in additional collateral, while JPM maintained it acted in good faith to manage growing exposure amid deteriorating collateral liquidity and overstated valuations.

Topic 1. Repos During the Credit Crisis

-

Bear Stearns:

-

Shift in funding model: Prior to 2007, Bear Stearns relied mainly on short-term unsecured commercial paper but later shifted toward longer-term, secured repo financing using high-quality collateral to improve funding stability.

-

Market stress response: During the crisis, lenders became reluctant to provide repo funding—especially term repos—leading to shorter tenors, higher haircuts, and stricter collateral requirements.

-

Run and collapse: In March 2008, a loss of market confidence triggered a run on Bear Stearns, with lenders refusing to roll repos and withdrawing liquidity, ultimately causing the firm’s rapid collapse.

-

Topic 2. Collateral in Repo Transactions

- There are two main types of collateral used in repos: general collateral (GC) and special collateral.

-

General Collateral (GC): In GC repos, lenders specify only broad categories of acceptable collateral and do not require a specific security, avoiding scarcity-driven pricing effects.

-

GC rate: The repo rate for trades secured with general collateral.

-

Return implications: As GC repos do not create demand for a particular security, lenders earn higher repo rates compared to special collateral trades, making GC attractive for investors.

-

Relation to policy rates: U.S. Treasury GC rates typically trade slightly below the federal funds rate, and the fed funds–GC spread widens when Treasuries are scarce or during periods of financial stress.

-

-

Special Collateral: When a repo is done to obtain a specific security as collateral, it is called a specials trade, and the associated repo rate is the special rate.

-

Financing motivation: Specials trades are used to finance short positions, inventory, or proprietary bond positions where access to a particular security matters more than the cash rate.

-

Below-GC trade-off: Lenders accept lending cash at rates below GC in exchange for receiving the desired security as collateral.

-

Security-specific pricing: Special rates vary by security and tenor and are driven by supply and demand in the specials market, which can differ from demand for the bond in the cash market.

-

Practice Questions: Q1

Q1. In a presentation to management, a bond trader makes the following statements about repo collateral:

- Statement 1: "The difference between the federal funds rate and the general collateral rate is the special spread."

- Statement 2: "During times of financial crises, the spread between the federal funds rate and the general collateral rate widens."

Which of the trader’s statements are accurate?

A. Both statements are incorrect.

B. Only Statement 1 is correct.

C. Only Statement 2 is correct.

D. Both statements are correct.

Practice Questions: Q1 Answer

Explanation: C is correct.

The trader’s first statement is incorrect. The difference between the federal funds rate and the general collateral (GC) rate is known as the fed funds-GC spread. The special spread is the difference between the GC rate and the special rate for a particular security. The trader’s second comment is correct. During times of financial crises, the spread between the federal funds rate and the general collateral rate widens as the willingness to lend Treasury securities declines, lowering the GC rate (there by increasing the spread).

Topic 3. Special Spreads and the Auction Cycle

-

Special Spread: Difference between the GC rate and the special rate for a particular security and term.

-

Special spreads are important because in the U.S., they are tied closely to the U.S. government T-bond auctions, and the level and volatility of the spread can be an important gauge of market sentiment.

-

-

OTR and OFR Issues: U.S. government bonds are issued on a fixed auction schedule, with the most recent issue designated as on-the-run (OTR) and earlier issues classified as off-the-run (OFR).

-

Liquidity of OTR issues: OTR Treasuries are the most liquid, with tight bid–ask spreads and easy execution in large sizes, making them attractive for both long and short positions.

-

Their heavy use as special collateral in repos has historically led to lower repo rates and wider special spreads.

-

- Volatility and time variation: OTR special spreads can be volatile on a daily basis and fluctuate over time depending on the availability and demand for specific collateral.

-

Auction-driven pattern: Special spreads are typically narrow immediately after auctions due to increased supply of the new OTR issue, and widen ahead of auctions as scarcity increases and shorts shift toward the next OTR security.

-

Term structure effect of auctions: Term special spreads for OTR issues typically decline immediately after a new auction due to increased supply and then rise as the next auction approaches and the security becomes scarcer.

Topic 4. Special Spreads and Rate Levels

- Bounds on special spreads: Special spreads are capped by the GC rate and floored at zero, since traders will not borrow bonds at negative special rates; in settlement fails, borrowing at a 0% special rate effectively provides free financing to obtain the bond.

- Penalty-driven upper limit: Post-2009 fail penalties, set as max(3%3\%3% - fed funds rate, 0), impose an upper bound on special spreads, with the cap tightening as policy rates rise and reaching a maximum when rates are near zero.

Topic 5. Financing Advantage of a Bond Trading Special

-

The premium trading value of OTR bonds is due both to their liquidity and financing advantage.

-

Liquidity advantage: These bonds can be quickly sold in the market to raise cash.

-

Financing value: Lending the bonds at a cheap special rate and the cash is lend out at higher GC rates.

-

- Time-dependent financing value: The value depends on how long the bond is expected to trade at a special rate before converging toward the GC rate

-

Example: Let’s assume that an OTR bond is issued on January 1 and trades at a special spread of 0.18%. A trader expects the bond to trade at GC rates past March 31. The financing value of the OTR bond is therefore the value over 90 days. The value of $100 of cash at the spread of 0.18% is:

-

- Thus, the financing value is 4.5 cents per $100market value of the bond.

\begin{aligned}

\text { Financing Value }&=\text { (Cash Amount) } \times \frac{\text { (Days of Financing) } \times \text { (Special Spread) }}{360}\\

\text{Financing Value }&=\$ 100 \times \frac{(90 \times 0.18 \%)}{360}=\$ 0.045

\end{aligned}

Practice Questions: Q2

Q2. The latest on-the-run (OTR) Treasury bond issued on March 1 is trading at a special spread of 0.25%. Traders expect the bond to trade at general collateral (GC) rates past June 30. The financing value of the OTR bond is therefore the value over 122 days. Given this information, the value of lending $100 of cash is closest to:

A. $0.085.

B. $0.250.

C. $0.305.

D. $0.847.

Practice Questions: Q2 Answer

Explanation: A is correct.

The financing value of $100 of cash at a spread of 0.25% is calculated as:

\$ 100 \times \frac{122 \times 0.25 \%}{360}=\$ 0.0847 \text { or } 8.47 \text { cents }

Copy of LTR 13. Repurchase Agreements and Financing

By Prateek Yadav